The traditional image of the Australian university student—clutching a physical wallet and stressing over a paper bank statement—has officially become a relic of the past. As we move through 2026, the intersection of higher education and financial technology (fintech) has reached a tipping point.

With the cost of living in hubs like Sydney and Melbourne continuing to challenge student budgets, the Australian “Gen Zalpha” cohort has turned to sophisticated digital tools to keep their heads above water. From AI-driven budgeting apps to decentralized micro-lending, fintech is no longer just a convenience; it’s a survival strategy.

The 2026 Landscape: Why Fintech?

According to recent data from the Australian Bureau of Statistics (ABS) and Fintech Australia, over 88% of tertiary students now utilize at least three distinct fintech platforms to manage their daily lives. The primary drivers are twofold: the eradication of traditional banking fees and the need for real-time expense tracking in an era of fluctuating inflation.

In 2026, the “Bank of Mum and Dad” has been replaced by peer-to-peer (P2P) lending circles and automated “round-up” savings tools. Students are no longer just passive spenders; they are micro-investors and hyper-efficient budgeters.

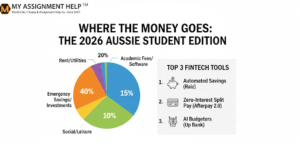

Balancing the Books: Education vs. Living Costs

The modern student’s budget is a complex puzzle. Between skyrocketing textbook subscriptions, specialized software fees, and the ever-present rent, many find themselves stretched thin. To maintain their GPAs without crashing financially, students are prioritizing “outsourcing” their time.

For instance, when deadlines pile up, many choose to invest in professional assignment help Australia to ensure they don’t fail a unit—a mistake that costs thousands in repeated tuition fees. By using fintech tools to save on daily coffee or transport, students reallocate those funds into academic support services that guarantee a better ROI on their degree.

Top Fintech Trends Dominating Australian Campuses in 2026

1. AI-Powered Predictive Budgeting

Gone are the days of manual spreadsheets. Apps like Up, PocketSmith, and new AI-integrated versions of CommBank’s app now predict a student’s “Safe-to-Spend” limit by analyzing upcoming bills, grocery habits, and even HECS-HELP indexation rates. These apps send “nudge” notifications before a student overspends on a night out in Fortitude Valley or Carlton.

2. Micro-Invoicing for the Gig Economy

Many Australian students in 2026 are “Side-Hustlers.” Whether they are selling digital art, tutoring, or doing freelance coding, fintech platforms now allow them to issue instant invoices and receive payments in multiple currencies with near-zero fees. This liquidity allows students to pay someone to do assignment tasks or complex research during peak exam periods, effectively trading a few hours of freelance income for academic peace of mind.

3. Fractional Investing and “Round-Ups”

Micro-investing apps like Raiz and Spaceship have evolved. In 2026, these platforms allow students to “round up” their purchase of a $5.50 Flat White to $6.00, investing the change into “Education ETFs.” Over a three-year degree, these cents accumulate into a significant fund that many use to pay off their student union fees or graduation costs.

The Rise of “Study-Now-Pay-Later” (SNPL)

While Buy-Now-Pay-Later (BNPL) started with fashion, 2026 has seen the maturation of Study-Now-Pay-Later. This specialized fintech niche allows students to spread the cost of high-ticket academic items—like high-end laptops for Architecture students or professional certification courses—over a semester without the predatory interest rates of traditional credit cards.

This trend reflects a broader shift in Australian culture: viewing education as a modular investment rather than a one-time debt.

Key Takeaways for Students

- Automation is King: Set up “buckets” or “envelopes” in your banking app to automatically sequester rent money the moment your pay or Centrelink hits.

- Leverage Student Discounts via Fintech: Many neobanks now offer integrated cashback rewards specifically for student-heavy retailers and academic services.

- Protect Your Credit Score: While BNPL and SNPL are tempting, ensure you use them responsibly to build a credit history that will help you buy a home post-graduation.

- Invest in Time: Use your fintech savings to buy back your time. Outsourcing repetitive tasks can prevent burnout and improve academic outcomes.

FAQ Section

Q: Are fintech apps safe for Australian students?

A: Yes, most Australian fintechs are regulated by ASIC and APRA. Always ensure the app has an Australian Financial Services Licence (AFSL).

Q: Can fintech help me pay off my HECS-HELP debt faster?

A: Some apps now allow you to make voluntary contributions by “rounding up” your daily spending, which can help reduce the principal before indexation hits on June 1st each year.

Q: Do these apps charge monthly fees?

A: Most student-focused neobanks offer zero-fee accounts, provided you are a full-time student or under a certain age (usually 25-30).

Q: Is it ethical to use academic support services found through fintech savings?

A: Absolutely. Using professional services for guidance and tutoring is a common way for students to manage high workloads, provided they use the materials as a study reference.

About the Author: Sarah Jenkins

Sarah Jenkins is a Senior Academic Consultant at MyAssignmentHelp. With over a decade of experience in the Australian higher education sector, Sarah specializes in student welfare and financial literacy. She has helped thousands of students navigate the pressures of university life by combining academic excellence strategies with modern digital tools. When she’s not writing, Sarah explores the latest in DeFi and its applications for international students in Australia.

References:

- Fintech Australia (2025 Annual Census). 2. Reserve Bank of Australia (RBA) – Digital Payments Evolution Report 2026.

- Universities Australia – Student Financial Stress Indicators 2026.

- ASIC MoneySmart – Managing Money as a Tertiary Student.

Conclusion

The Australian student of 2026 is more financially literate than any generation prior. By embracing fintech, they are turning the “struggling student” trope on its head. Through a combination of AI budgeting, smart micro-investing, and strategic spending on academic support, they are navigating the high cost of education with unprecedented precision.

{kind=link}